Hybrid Retirement Plan (DC Component)

The hybrid plan combines elements of a traditional defined benefit (DB) pension plan and a defined contribution (DC) plan that is similar to a 401(k).

It’s important to understand both components of your hybrid plan before we go into more specifics on the VRS Defined Contribution Plan (DCP) component.

Defined Benefit

- Provides the foundation of your future retirement benefit when you qualify.

- Pays a lifetime monthly retirement benefit based on age, total service credit and average final compensation.

- VRS manages the investments and related risk for this component.

Get more information on the Hybrid Plan Defined Benefit Component at varetire.org/hybrid.

Defined Contribution

- Provides a tax-deferred savings plan in addition to your defined benefit pension.

- Provides a balance to draw from during retirement. Your balance is based on contributions by you and your employer to the plan and the investment performance of those contributions.

- You manage the investments and related risk for this component.

Visit the Hybrid Learning Channel to learn more about the hybrid plan features and benefits.

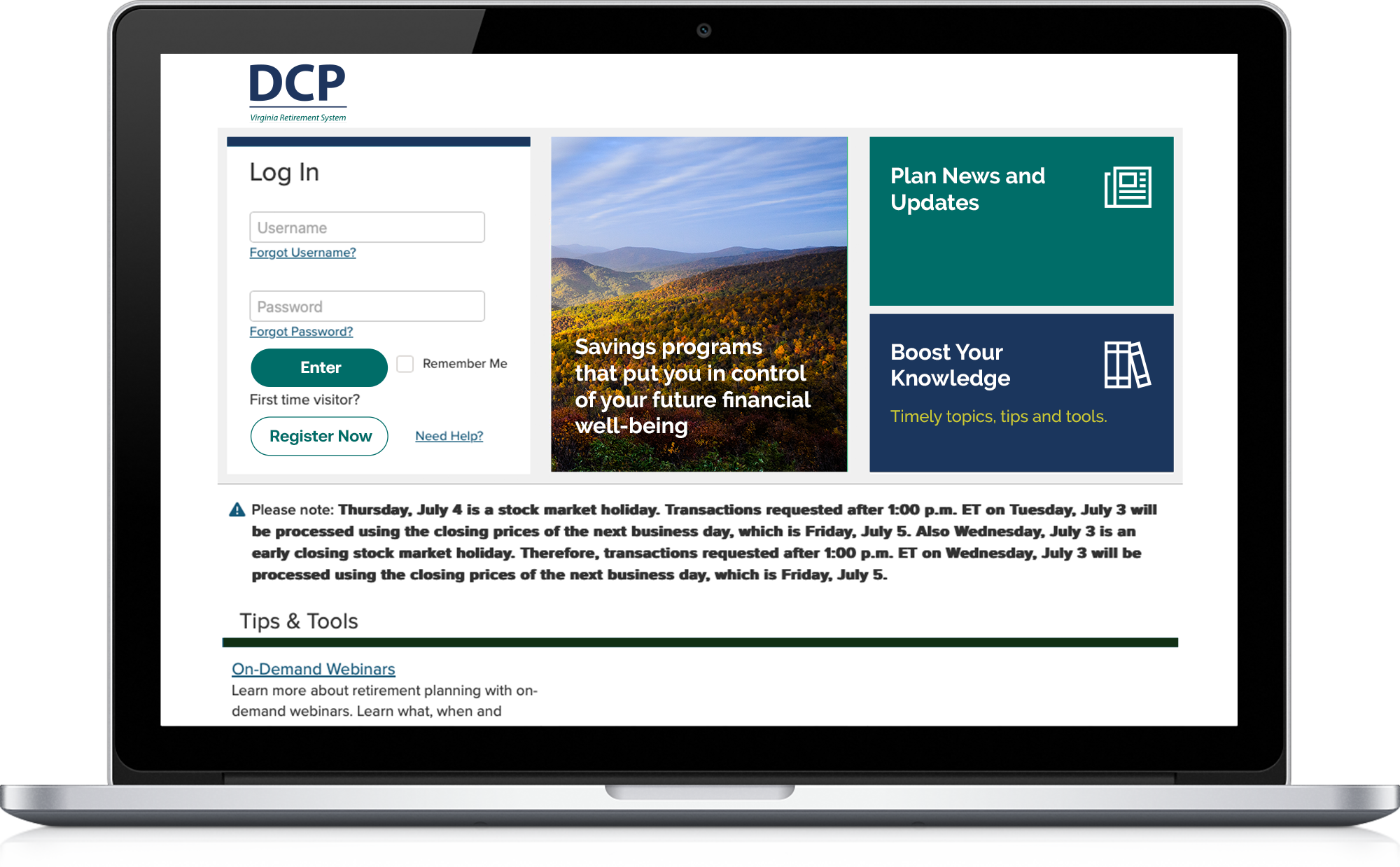

Jump start your financial future, today.

Log in now to the DC component of your Hybrid Retirement Plan to help realize your retirement goals. If you are already saving, take action to manage your account.

DCP Account

How to contribute

How to contribute

IRS Contribution Limits

Investment Options

Withdrawing money

Vesting

Naming beneficiaries

Statements and confirmations

Fees and expenses

Leaving employment

News and insights

Focus Newsletters

Get the latest news and insights on your VRS Defined Contribution Plans.

Retirement Planning for Women

Join us to explore retirement strategies, investment options and real‑life insights designed to meet women where they are in their financial journey.

Tools & Resources

Access digital educational tools and resources to help you gain better money habits and plan your financial future.

Navigating Market Volatility

Learn how to better navigate the ups and downs of today's markets.

Reading Your Statement

Review this guide to understanding your Voya® account statement.

Need Help?

Locate and contact your DC Plans Education Specialist to schedule one-on-one counseling.